I gave Claude three years of annual reports from Titan Company Ltd. — one of India's leading jewellery and watch companies — and asked it to build a financial model from scratch. In under five minutes, I had a working eight-tab spreadsheet on my screen. The question was whether it was any good.

Financial modelling is the backbone of investment analysis, credit assessment, and corporate valuation. Building a robust model typically takes hours — sometimes days — as analysts gather data, structure assumptions, link financial statements, and develop forecasting drivers. With recent advances in generative AI, a natural question arises:

Can AI build a financial model in minutes?

To find out, I ran a practical experiment using Claude (Opus 4). Along the way, I tried something I hadn't planned: I asked a second AI to critique the first one's work. What emerged was a window into where modelling stands in the AI era — what's becoming automated, and what still requires human judgement.

The results were both impressive and revealing.

Step 1: The First Draft

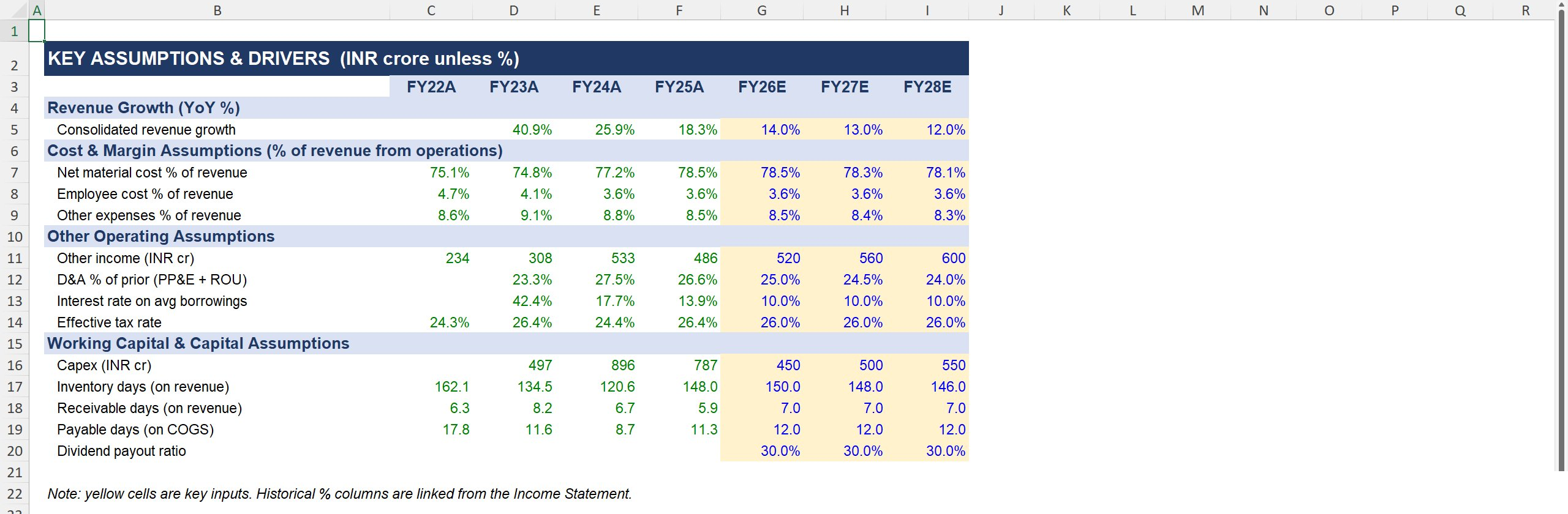

Within minutes, Claude produced a working financial model containing eight tabs: Cover, Assumptions, Income Statement, Balance Sheet, Cash Flow Statement, Segment Analysis, Ratios, and Standalone P&L.

At first glance, this was a remarkably good start — well organised, with all the key financial statements and supporting schedules an analyst would expect. But looking beyond the structure, limitations emerged.

What Claude Got Right

The model successfully extracted historical financial data, structured the three financial statements, calculated key ratios, created a forecast framework, and produced a coherent Excel model architecture. For a task that would typically take a junior analyst several hours, the productivity gain was significant.

Where Claude Fell Short

The assumptions driving the forecast were relatively simplistic. Revenue growth, margins, working capital, capex and debt assumptions were largely projected using historical trends and high-level percentage assumptions — revenue growth assumed directly, inventory days as static percentages, capex as broad estimates, and debt balances without detailed financing schedules.

The model answered the question of what might happen, but not why it might happen. In professional modelling, that distinction matters.

Step 2: Adding Segment-Level Forecasting

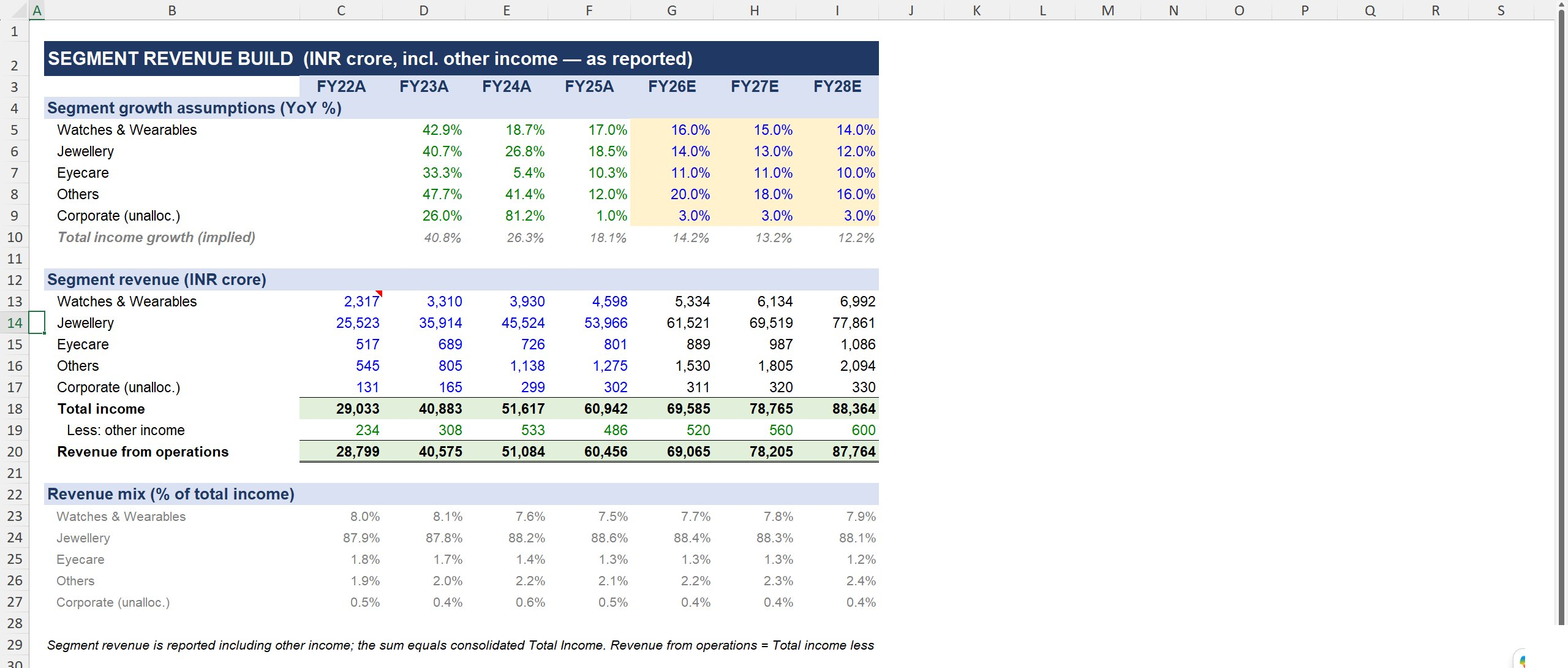

To improve the model, I asked Claude to identify Titan's underlying revenue drivers and incorporate them into the forecast. Claude responded by creating a new "Revenue Build" tab that forecast revenue by business segment: Jewellery, Watches & Wearables, Eyecare, and Other Businesses.

This was a meaningful improvement. The model now forecast revenue at a segment level rather than using a single consolidated growth assumption.

However, the forecasts were still largely assumption-based. Segment revenues were projected using assumed growth rates rather than operational drivers. The model had become more granular, but not necessarily more analytical.

Step 3: Using AI to Critique AI

At this stage, I became curious. Could a second AI identify weaknesses in the first AI's model?

I uploaded the model to Microsoft Copilot and asked it to review the structure and suggest improvements. The results were surprisingly useful. Rather than rebuilding the model, Copilot acted like an experienced modelling reviewer, highlighting several areas where the forecast framework could be strengthened.

Key Recommendations

Revenue Forecasting

Copilot suggested linking segment growth directly to operational drivers — store count, same-store sales growth, average selling prices, and gold price movements. It also recommended separating revenue from other income and adding reconciliation checks between segment forecasts and consolidated financial statements.

Working Capital

Instead of using flat inventory, receivable and payable days, Copilot suggested linking inventory levels to gold price volatility, receivables to credit sales mix, and payables to supplier terms.

Capex

Rather than applying simple growth assumptions, capex could be split into maintenance capex, expansion capex, and strategic investments — providing greater visibility into the drivers of future growth.

Debt and Financing

Copilot also highlighted the need to separate gold-on-loan financing from conventional borrowings, create debt maturity schedules, and link borrowing requirements to inventory growth and expansion plans.

These were all sensible recommendations that an experienced modelling professional would likely make.

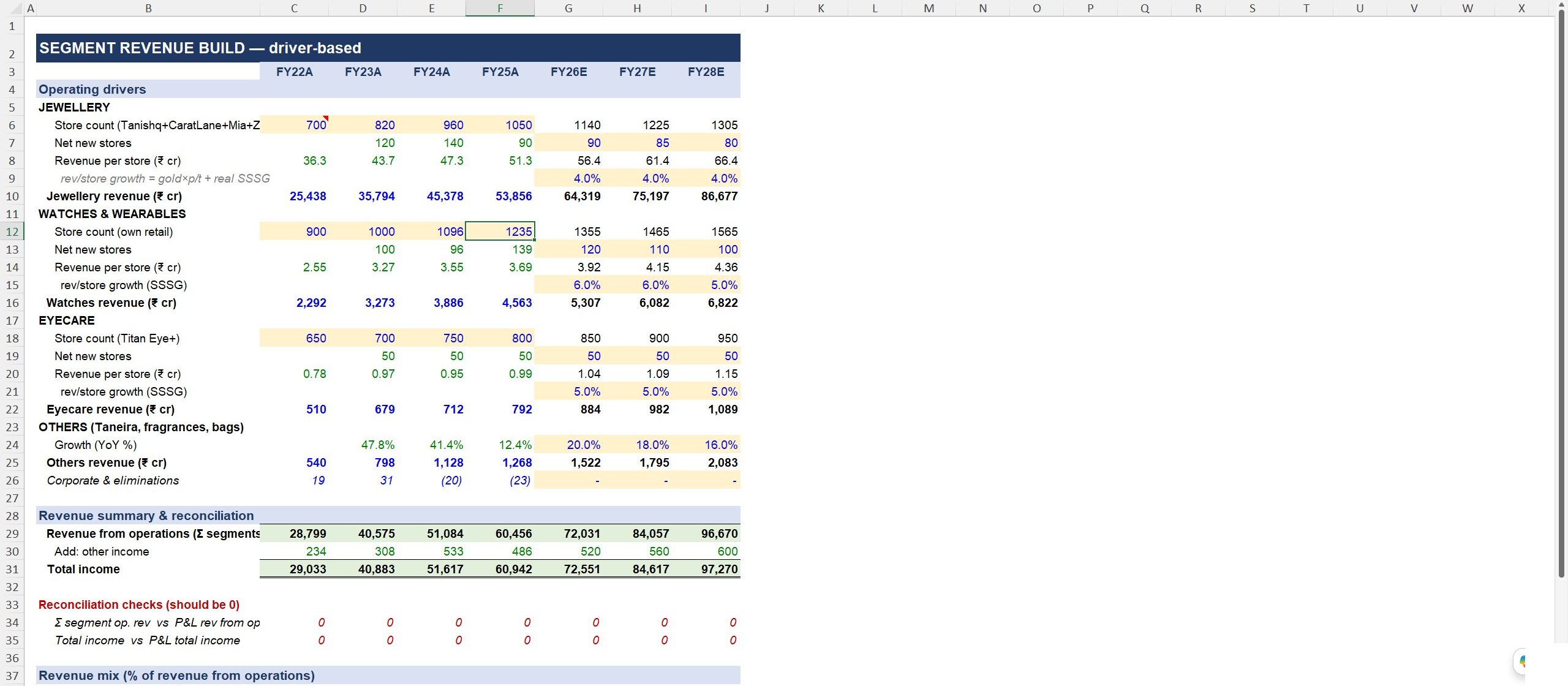

Step 4: Building Version 3

I fed these recommendations back into Claude and asked it to improve the model. The result was Version 3 — adding driver-based revenue forecasting, capex schedules, debt schedules, revenue reconciliation checks, and more detailed operational assumptions.

Most importantly, the revenue forecast became linked to business drivers.

Jewellery Revenue Example

Instead of simply assuming a growth rate, the jewellery forecast was built using store count, net store additions, revenue per store, and same-store sales growth assumptions. This is much closer to how an analyst would actually forecast a retail business.

Similarly, the watches and eyewear segments were linked to store expansion and productivity assumptions. The model also introduced reconciliation checks to ensure that segment forecasts tied back to the consolidated income statement.

This was a substantial improvement over the original version.

What AI Still Misses

Despite the progress, the exercise highlighted an important limitation.

Are management's growth targets realistic? Is jewellery market growth sustainable? Will gold prices affect consumer demand? Are store expansion assumptions achievable? Is management allocating capital effectively?

These questions require business judgement rather than spreadsheet construction. The mechanical process of modelling can increasingly be automated. The analytical process remains much harder to replicate.

Key Lessons

After three iterations, several conclusions became clear.

1. AI is already a powerful modelling assistant

Claude produced a workable financial model in minutes. The productivity gain is real.

2. Prompting matters

The quality of the model improved significantly with each round of feedback. The first answer was never the final answer.

3. Multiple AI tools can work together

Using one AI to generate the model and another to critique it proved surprisingly effective. This created an iterative review process similar to what happens within investment banks, credit teams, and consulting firms.

4. Driver-based modelling remains critical

The biggest improvement came when forecasts were linked to operational drivers rather than simple growth assumptions. This remains a fundamental principle of good financial modelling.

5. Human judgement is still essential

AI can build the structure. AI can suggest improvements. AI can accelerate the process dramatically. But analysts still need to determine whether the assumptions are reasonable and whether the story being told by the numbers is credible.

Final Verdict

Can AI build a financial model? The answer is clearly yes.

Can AI build a detailed, reliable working model without human input? Not yet.

What this experiment demonstrated is that AI can dramatically reduce the time spent on the mechanical aspects of model construction. Instead of starting from a blank spreadsheet, analysts can start from a functioning model and focus their efforts on refining assumptions, testing scenarios, and developing investment insights.

AI won't replace the financial modeller. But the modeller who learns to use it well will quietly replace the one who doesn't.